Special Enforcement Section (SES) – Violations

Hawaii law authorizes the Special Enforcement Section to enforce Hawaii tax laws through the issuance of cease and desist citations, which can include substantial monetary fines. The following are offenses citable by the SES –

| Failure to: | A violation of this provision results in a fine not to exceed: | |

|---|---|---|

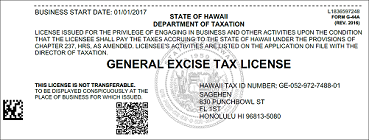

| Produce license upon demand Every person required to be licensed or permitted under Hawaii tax law is required to produce their license upon demand by the SES. |

$500 for most persons $1,000 for cash-based businesses |

|

|

Obtain a GE license | $500 for most persons $2,000 for cash-based businesses |

|

Keep adequate books and records Every person doing business in Hawaii is required to keep adequate books and records in order to show taxable receipts, deductions, credits, and other assessments or adjustments to their tax. |

$1000 for most persons $2,000 for cash-based businesses |

|

Record transaction

It is unlawful for any person doing business to conduct any transaction in cash and fail to: |

$1000 for most persons $2,000 for cash-based businesses |

| Tax avoidance price fixing Persons who offer price differentials where the transaction is paid in cash may violate the offense of tax avoidance price fixing. However, there is no violation where there are legitimate business purposes for offering two prices for a transaction occurring in cash, such as for credit card fee recovery. |

$2000 for most persons $3,000 for cash-based businesses |

|

|

Possession of currency for tax avoidance purposes Where a person possesses cash with a purpose of avoiding taxes, the violation of possession of currency for tax avoidance purposes occurs. |

$2000 for most persons $3,000 for cash-based businesses |

|

Interference with a tax official It is unlawful for any person to interfere with, hinder, obstruct, prevent, or impede investigators of the SES or other Department of Taxation employee in furtherance of obtaining information or property rightfully entitled the Department. However, a person does not commit this violation where they act with good cause. |

$2000 for most persons $3,000 for cash-based businesses |

Poster

- Does your business involve “cash” transactions? (PDF) July 30, 2013, one 8-1/2 x 11 page, 209 KB

- Does your business involve “cash” transactions? (PDF) [ Chinese ]

July 30, 2013, one 8-1/2 x 11 page, 288 KB - Does your business involve “cash” transactions? (PDF) [ Korean ]

July 30, 2013, one 8-1/2 x 11 page, 257 KB

The SES is authorized to issue increased fines for persons found to be operating “cash-based businesses.” A cash-based business is defined as a person who operates a business, including for-profit and not-for-profit, where transactions in goods or services are exchanged substantially for cash and where the business is found to have met one or more of the following factors, which include:

- Substantially underreporting or misreporting the proper amount of tax liability on any tax return;

- Failing to have a license or permit as required by law;

- Having no fixed and permanent principal place of business; or

- Not accepting checks or electronic payment devices for business transactions.

The Director of Taxation is authorized to issue additional factors that the SES may consider when characterizing a business as a cash-based business through Tax Information Release.

See also:

Special Enforcement Section (SES) – Mission

Special Enforcement Section (SES) – Overview

Special Enforcement Section (SES) – Violations Enforced by SES

Special Enforcement Section (SES) – Contact SES

Page Last Updated: July 8, 2022